Introduction

One of the strongest features of the mlmodels package is

its unified predict() method. No matter which model you fit

(ml_lm, ml_poisson, ml_negbin,

ml_logit, ml_beta, etc.), you can obtain

predictions and standard errors using the same consistent interface.

This vignette shows how to use predict() directly, then

demonstrates how mlmodels integrates with the excellent marginaleffects

package for average predictions, marginal effects, and more.

The predict() Method

The predict() function in mlmodels returns

an object of class predict.mlmodel, which is a list

composed of two elements:

-

fit: the predicted values. -

se.fit: standard errors calculated via the delta method using analytical gradients (only present ifse.fit = TRUE).

By default, predict() returns in-sample

predictions. It automatically aligns the results to the

original dataset, inserting NA for observations that were

dropped during estimation (due to missing values, subsetting, or invalid

outcome values for the specific model, such as non-positive values in

gamma and lognormal models, or values outside (0,1) in beta

regression).

Basic Usage

data(mroz)

mroz$incthou <- mroz$faminc / 1000

fit <- ml_lm(incthou ~ age + I(age^2) + educ + kidslt6, data = mroz)

# Default: expected value (response)

pred <- predict(fit)

head(pred$fit)

#> [1] 19.74355 18.70671 21.28132 20.98756 23.15382 23.17217

# With standard errors

pred_se <- predict(fit, se.fit = TRUE)

head(data.frame(fit = pred_se$fit, se = pred_se$se.fit))

#> fit se

#> 1 19.74355 0.8506750

#> 2 18.70671 1.2325354

#> 3 21.28132 0.7538523

#> 4 20.98756 0.7605700

#> 5 23.15382 0.9533716

#> 6 23.17217 0.7866816Predicting for Different Models

The usage of the predict() function is the same for

different models, only that different models have different types of

predictions, since they have different parameters.

# Linear model

pred_lm <- predict(fit)

head(pred_lm$fit)

#> [1] 19.74355 18.70671 21.28132 20.98756 23.15382 23.17217

# With standard errors (robust)

pred_lm_se <- predict(fit, vcov.type = "robust", se.fit = TRUE)

head(data.frame(fit = pred_lm_se$fit, se = pred_lm_se$se.fit))

#> fit se

#> 1 19.74355 0.9809821

#> 2 18.70671 0.9734422

#> 3 21.28132 0.9650118

#> 4 20.98756 0.6138107

#> 5 23.15382 1.1163924

#> 6 23.17217 0.7259417

# Poisson model

pois <- ml_poisson(docvis ~ age + educyr + totchr, data = docvis)

pred_pois <- predict(pois)

head(pred_pois$fit)

#> [1] 10.169550 6.266430 6.795981 9.255944 5.471075 5.002632

pred_pois_prob <- predict(pois, type = "P(0)") # Probability of zero

head(pred_pois_prob$fit)

#> [1] 3.831957e-05 1.898996e-03 1.118260e-03 9.554204e-05 4.206705e-03

#> [6] 6.720233e-03

# Negative Binomial (NB2)

nb2 <- ml_negbin(docvis ~ age + educyr + totchr, data = docvis)

pred_nb <- predict(nb2)

head(pred_nb$fit)

#> [1] 10.580216 6.312773 6.843628 9.521127 5.323215 4.818987

pred_nb_var <- predict(nb2, type = "variance")

head(pred_nb_var$fit)

#> [1] 84.17289 32.51184 37.63424 69.11783 23.95239 20.08610

# Beta regression (fractional response)

beta <- ml_beta(prate ~ mrate + age,

scale = ~ sole + totemp,

data = pw401k,

subset = prate < 1)

#> ℹ Improving initial values by scaling (factor = 0.5).

#> ℹ Initial log-likelihood: -282.46

#> ℹ Final scaled log-likelihood: 68.008

pred_beta <- predict(beta)

head(pred_beta$fit)

#> [1] 0.7552359 0.7987456 NA 0.7642674 0.7504521 NA

pred_beta_phi <- predict(beta, type = "phi") # Precision parameter

head(pred_beta_phi$fit)

#> [1] 6.773664 6.684076 NA 6.727120 6.727120 NANotice that the beta model predictions contain NA

values. These correspond to observations that we left out of the

estimation (subset = prate < 1), because the Beta model

only takes true fractional responses.

You can always do out-of-sample predictions, by

passing the full dataset via the newdata argument:

pred_beta <- predict(beta, newdata = pw401k)

head(pred_beta$fit)

#> [1] 0.7552359 0.7987456 0.8084212 0.7642674 0.7504521 0.8538617The NA values are now replaced with predictions for the

previously excluded observations.

For a complete list of supported prediction types for each model family, see the detailed tables in the help page:

?predict.mlmodelComparison with predictions() from

marginaleffects

As we’ve explained before, we have made our package compatible with

marginaleffects, which provides powerful tools for

post-estimation analysis.

There are several distinctions between our predict() and

predictions(), from marginaleffects, that are

worth understanding:

-

predict()uses analytical gradients for its delta-method standard errors and defaults to in-sample predictions, automatically aligning results to the original dataset (insertingNAs for dropped observations). -

predictions()uses numerical gradients for its delta-method standard errors. Withmlmodelsit also defaults to in-sample predictions, but but returns a reduced dataset by default, containing only the observations used in estimation. - Both functions can perform out-of-sample

predictions by passing the full dataset via the

newdataargument. -

predict()provides delta-method standard errors using any variance type supported bymlmodels(oim,opg,robust,boot,jack, etc.). -

predictions()uses the same delta-method approach by default and can take advantage of most of our variance types directly through thevcovargument. The only exception isvcov = "boot", which has a special meaning inmarginaleffects(see the bootstrapping section below). - You can also pre-compute any of our variance

matrices (including bootstrapped and jackknifed), using

vcov(), and pass the resulting matrix topredictions()through thevcovargument. This is especially recommended for bootstrapped and jackknifed standard errors when you plan to compute multiple predictions or marginal effects. -

predictions()also offers additional uncertainty methods — such as estimate bootstrap, simulation (Krinsky-Robb),rsample, etc. — which you can control more through itsinferences()function.

We start illustrating the relationship with a simple prediction with robust standard errors.

# Using our predict() function

our_pred <- predict(fit,

vcov.type = "robust",

se.fit = TRUE)

# Using marginaleffects::predictions()

me_pred <- predictions(fit,

vcov = "robust")

# Compare first 8 observations

comp <- data.frame(

obs = 1:8,

our_fit = our_pred$fit[1:8],

our_se = our_pred$se.fit[1:8],

me_fit = me_pred$estimate[1:8],

me_se = me_pred$std.error[1:8]

)

comp

#> obs our_fit our_se me_fit me_se

#> 1 1 19.74355 0.9809821 19.74355 0.9809816

#> 2 2 18.70671 0.9734422 18.70671 0.9734422

#> 3 3 21.28132 0.9650118 21.28132 0.9650113

#> 4 4 20.98756 0.6138107 20.98756 0.6138107

#> 5 5 23.15382 1.1163924 23.15382 1.1163919

#> 6 6 23.17217 0.7259417 23.17217 0.7259416

#> 7 7 30.29423 1.0659127 30.29423 1.0659127

#> 8 8 23.17217 0.7259417 23.17217 0.7259416As you can see, the predicted values are exactly the same,

since they both come from our predict()

function, and the standard errors are extremely close —

differing only in the later decimal places. This illustrates that for

practical inference purposes, both approaches are equally valid. The

small differences arise because predict() uses analytical

gradients while predictions() uses numerical gradients by

default.

In-Sample and Out-of-Sample Predictions

As mentioned, with mlmodels both predict()

and predictions() default to in-sample

predictions (only using observations that were included in

model estimation).

However, they return different sized data frames:

# Beta model fitted on a subset (prate < 1)

beta <- ml_beta(prate ~ mrate + age,

scale = ~ sole + totemp,

data = pw401k,

subset = prate < 1)

#> ℹ Improving initial values by scaling (factor = 0.5).

#> ℹ Initial log-likelihood: -282.46

#> ℹ Final scaled log-likelihood: 68.008

# Our predict() - returns full length with NAs

our_beta <- predict(beta, se.fit = TRUE, vcov.type = "robust")

# marginaleffects::predictions() - returns reduced dataset

me_beta <- predictions(beta, vcov = "robust")

# Compare frst 8 observations

head(data.frame(Estimate = our_beta$fit, Std.Error = our_beta$se.fit), 8)

#> Estimate Std.Error

#> 1 0.7552359 0.004104833

#> 2 0.7987456 0.004631183

#> 3 NA NA

#> 4 0.7642674 0.003289174

#> 5 0.7504521 0.003836320

#> 6 NA NA

#> 7 0.7482266 0.004075500

#> 8 0.7431659 0.004416452

head(me_beta[, c("estimate", "std.error")], 8)

#>

#> Estimate Std. Error

#> 0.755 0.00410

#> 0.799 0.00463

#> 0.764 0.00329

#> 0.750 0.00384

#> 0.748 0.00408

#> 0.743 0.00442

#> 0.739 0.00444

#> 0.831 0.02209You can see that predict() returns predictions aligned

to the original dataset, inserting NA for observations that

were dropped during estimation, whereas predictions() is

missing those observations, returning a data frame containing only the

observations actually used in the model.

Out-of-Sample Predictions

To obtain predictions on the full original dataset (out-of-sample),

simply pass the complete data via the newdata argument in

either function:

# Out-of-sample with our predict()

our_full <- predict(beta, newdata = pw401k, se.fit = TRUE, vcov.type = "robust")

# Out-of-sample with marginaleffects

me_full <- predictions(beta, newdata = pw401k, vcov = "robust")

# Compare first 8 observations

comp <- data.frame(

obs = 1:8,

our_fit = our_full$fit[1:8],

our_se = our_full$se.fit[1:8],

me_fit = me_full$estimate[1:8],

me_se = me_full$std.error[1:8]

)

comp

#> obs our_fit our_se me_fit me_se

#> 1 1 0.7552359 0.004104833 0.7552359 0.004104833

#> 2 2 0.7987456 0.004631183 0.7987456 0.004631184

#> 3 3 0.8084212 0.004472564 0.8084212 0.004472565

#> 4 4 0.7642674 0.003289174 0.7642674 0.003289174

#> 5 5 0.7504521 0.003836320 0.7504521 0.003836321

#> 6 6 0.8538617 0.006884965 0.8538617 0.006884966

#> 7 7 0.7482266 0.004075500 0.7482266 0.004075501

#> 8 8 0.7431659 0.004416452 0.7431659 0.004416453Once more they’re both aligned and close.

Aligning marginaleffects in-sample

predictions

If you want in-sample predictions from marginaleffects

but aligned to the original dataset (with NAs for dropped

observations), you can do the following:

# predict as if out-of-sample

me_outin <- predictions(beta, newdata = pw401k, vcov = "robust")

# replace the values for the observations that weren't used with NA

me_outin[!beta$model$sample, ] <- NA

# Compare first 8 observations with our in-sample

comp <- data.frame(

obs = 1:8,

our_fit = our_beta$fit[1:8],

our_se = our_beta$se.fit[1:8],

me_fit = me_outin$estimate[1:8],

me_se = me_outin$std.error[1:8]

)

comp

#> obs our_fit our_se me_fit me_se

#> 1 1 0.7552359 0.004104833 0.7552359 0.004104833

#> 2 2 0.7987456 0.004631183 0.7987456 0.004631184

#> 3 3 NA NA NA NA

#> 4 4 0.7642674 0.003289174 0.7642674 0.003289174

#> 5 5 0.7504521 0.003836320 0.7504521 0.003836321

#> 6 6 NA NA NA NA

#> 7 7 0.7482266 0.004075500 0.7482266 0.004075501

#> 8 8 0.7431659 0.004416452 0.7431659 0.004416453Every mlmodel object stores a logical vector called

sample inside model$sample. This vector

indicates which observations from the original dataset were actually

used during model estimation (TRUE) and which were dropped

(FALSE).

Bootstrap Inference

There are two main approaches to bootstrap-based inference:

- Bootstrapped variance + delta method - You compute a bootstrapped variance-covariance matrix, and use it calculate standard errors and confidence intervals (similar to how you do with the coefficients of the estimation).

- Full bootstrap of the quantity - You refit the model on many bootstrap samples, compute the prediction (or marginal effect) for each sample’s estimation, and then derive confidence intervals from the percentiles of that distribution.

marginaleffects uses the second

approach (full bootstrap of the predictions) when you specify

vcov = "boot" in any of its predicting functions, or when

you use inferences(method = "boot"). This method is

computationally heavier, but produces more robust confidence

intervals.

Since mlmodels also uses the string "boot"

as its option to get a bootstrapped variance, the only way to obtain

bootstrapped standard errors (approach 1) with

marginaleffects, is to pre-compute the

bootstrapped variance-covariance matrix with vcov(), and

pass it to predictions().

## 1st approach (Bootstrapped variance)

# pre-compute the variance on the linear model (low number of repetitions to make it fast)

v_boot <- vcov(fit, type = "boot", repetitions = 20, progress = FALSE)

# use it with predictions()

boot_delta <- predictions(fit, vcov = v_boot)

## 2nd approach (Bootstrapped prediction)

boot_pred <- predictions(fit) |>

inferences(method = "boot", R = 20) # Inferences allows you to set the repetitions.

# The estimate is the same in both methods

comp <- data.frame(

obs = 1:8,

Estimate = boot_delta$estimate[1:8],

Delta_Low = boot_delta$conf.low[1:8],

Delta_High = boot_delta$conf.high[1:8],

Pred_Low = boot_pred$conf.low[1:8],

Pred_High = boot_pred$conf.high[1:8]

)

comp

#> obs Estimate Delta_Low Delta_High Pred_Low Pred_High

#> 1 1 19.74355 17.74885 21.73825 18.03809 21.62272

#> 2 2 18.70671 16.48955 20.92387 17.16532 20.74261

#> 3 3 21.28132 19.25051 23.31213 19.51117 23.93240

#> 4 4 20.98756 19.63304 22.34208 20.08004 21.93223

#> 5 5 23.15382 20.71326 25.59439 21.45097 24.52777

#> 6 6 23.17217 21.92974 24.41460 21.66176 24.54116

#> 7 7 30.29423 28.61080 31.97765 28.48795 32.79090

#> 8 8 23.17217 21.92974 24.41460 21.66176 24.54116In the example we have used 20 repetitions, to speed up the illustration, and its building to satisfy CRAN’s requirements. But you should use at least 500 repetitions, in your actual work.

We see that the confidence intervals from both methods are very similar. In general, the full bootstrap approach (bootstrapping the predictions themselves) is more robust when the distributional assumptions of your model may not hold perfectly. This extra robustness comes at the cost of higher computational time compared to using a bootstrapped variance matrix with the delta method.

marginaleffects gives you the flexibility to choose

whichever approach best suits your needs and computational budget.

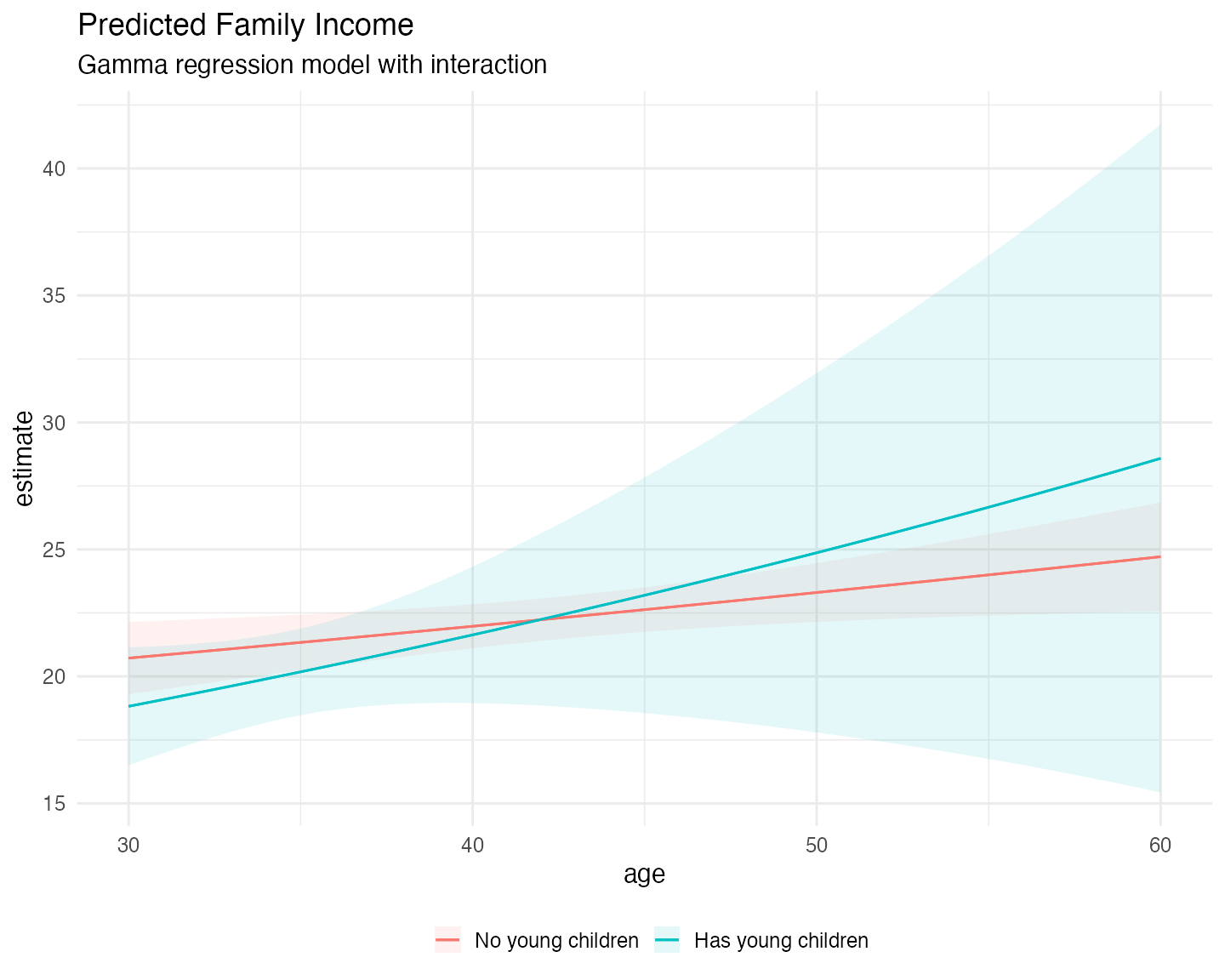

Interaction Effects and Plotting

One of the most useful features of marginaleffects is

its ability to visualize how effects vary across covariates. Here we fit

a Gamma model with an interaction between a binary indicator

(minors = has young children) and a continuous variable

(age):

# Create binary variable

mroz$minors <- factor(mroz$kidslt6 > 0,

levels = c(FALSE, TRUE),

labels = c("No young children", "Has young children"))

# Gamma regression with interaction

fit_gamma <- ml_gamma(incthou ~ age * minors + educ + hushrs,

data = mroz)

summary(fit_gamma, vcov.type = "robust")

#>

#> Maximum Likelihood Model

#> Type: Homoskedastic Gamma Model

#> ---------------------------------------

#> Call:

#> ml_gamma(value = incthou ~ age * minors + educ + hushrs, data = mroz)

#>

#> Log-Likelihood: -2762.37

#>

#> Wald significance tests:

#> all: Chisq(5) = 122.341, Pr(>Chisq) = < 1e-8

#>

#> Variance type: Robust

#> ---------------------------------------

#> Estimate Std. Error z value Pr(>|z|)

#> Value (incthou):

#> value::(Intercept) 1.601236 0.165711 9.663 < 2e-16 ***

#> value::age 0.005874 0.002310 2.543 0.011000 *

#> value::minorsHas young children -0.337768 0.342667 -0.986 0.324279

#> value::educ 0.082387 0.008567 9.617 < 2e-16 ***

#> value::hushrs 0.000117 0.000035 3.302 0.000959 ***

#> value::age:minorsHas young children 0.008056 0.009556 0.843 0.399215

#> Scale (log(nu)):

#> scale::lnnu 1.594196 0.067184 23.729 < 2e-16 ***

#> ---------------------------------------

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> ---

#> Number of observations:753 Deg. of freedom: 747

#> Pseudo R-squared - Cor.Sq.: 0.1545 McFadden: 0.02528

#> AIC: 5538.74 BIC: 5571.10

#> Shape Param.: 4.92 - Coef.Var.: 0.45Now we can use plot_predictions() to see the predicted

response for both groups at different ages:

# Load ggplot2 to plot with marginaleffects

library(ggplot2)

plot_predictions(fit_gamma,

condition = c("age", "minors"),

vcov = "robust") +

labs(title = "Predicted Family Income",

subtitle = "Gamma regression model with interaction",

color = "",

fill = "") +

theme_minimal(base_size = 15) +

theme(legend.position = "bottom")

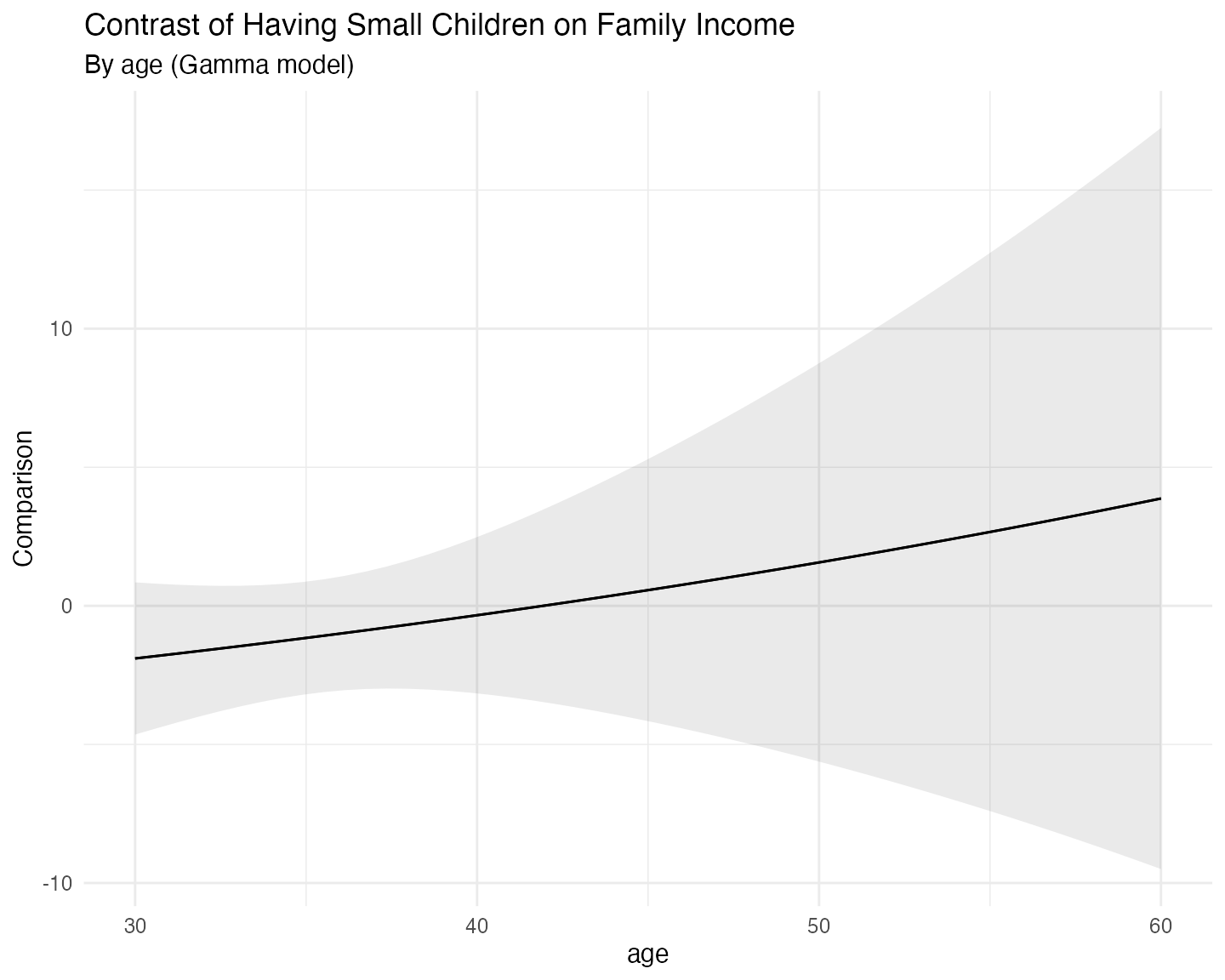

And we can do the same for the marginal effects:

plot_comparisons(fit_gamma,

variables = "minors",

condition = "age",

vcov = "robust") +

labs(title = "Contrast of Having Small Children on Family Income",

subtitle = "By age (Gamma model)") +

theme_minimal(base_size = 15)

Concluding Remarks

This vignette has demonstrated the unified predict()

method provided by mlmodels and its strong integration with

the marginaleffects

package.

Key takeaways include:

-

predict()offers analytical gradients and defaults to in-sample predictions with proper alignment (including NAs for dropped observations). -

predictions(), frommarginaleffects, also defaults to in-sample predictions withmlmodels, and uses numerical gradients that provide very precise standard erors, so for most applications it will be equivalent topredict(). - Both functions support out-of-sample predictions by supplying the

full original dataset via the

newdataargument. - You can obtain aligned in-sample predictions from

predictions()using thesamplelogical vector stored in everymlmodelobject. - The integration allows you to choose between fast delta-method

standard errors (using our variance estimators), and more robust full

bootstrap inference, or other methods of inference, via

inferences(). -

marginaleffectsfurther complementspredict()with powerful tools for average predictions, marginal effects, and interactions, and visualization.

Together, they provide a flexible and consistent workflow for

post-estimation analysis across all model families supported by

mlmodels.

For more details on specific prediction types, see

?predict.mlmodel. For more information about

marginaleffects, consult its excellent documentation.

Happy modeling!